Eight things to remember for 31 December 2024 annual reporting

Eight things to remember for 31 December 2024 annual reporting

This article highlights eight things to remember when preparing 31 December 2024 financial statements.

This article highlights eight things to remember when preparing 31 December 2024 financial statements. Entities should also consider continuing global geopolitical and economic uncertainty, including the impact of interest rate increases and inflation, and the effects those uncertainties might have when accounting for various items in your financial statements.

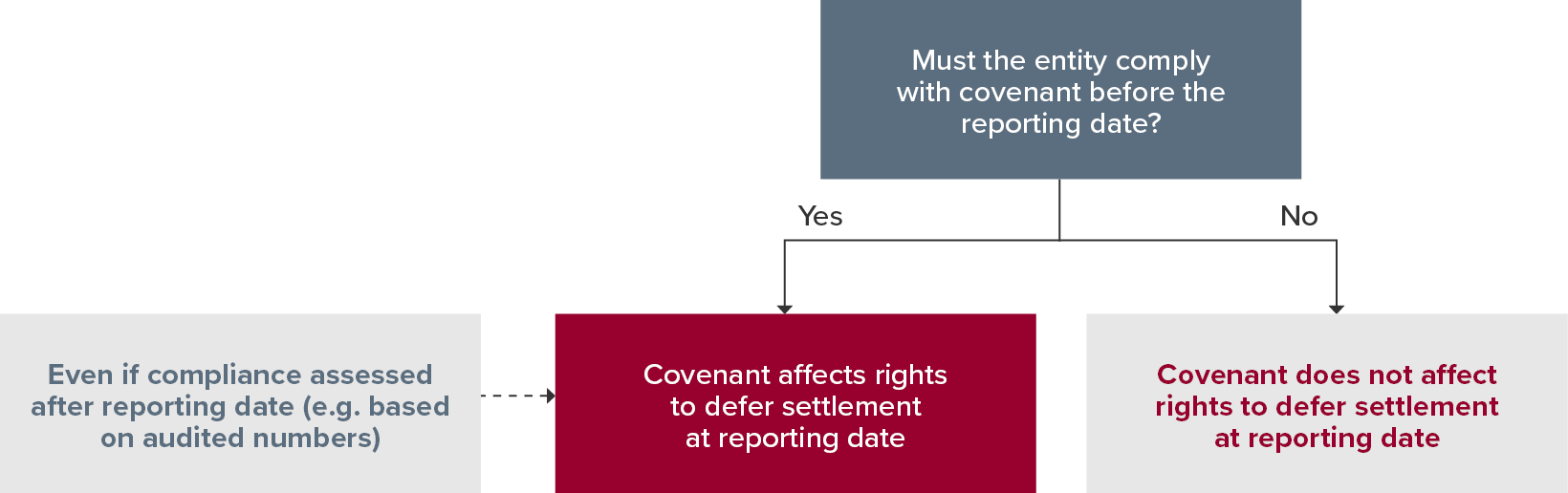

- Changes to classification requirements for liabilities

- Climate-related matters and mandatory sustainability reporting

- New standards applying for the first time to 31 December 2024 annual and half-year periods

- Pillar Two 'top-up' income taxes

- Recent agenda decisions

- Hyperinflationary economies

- Standards issued but not yet effective

- Material accounting policies.